Development and Innovation in the Five Major Formats of Internet Finance

In today’s dynamic financial ecosystem, the meteoric ascent of internet finance stands as a testament to the transformative power of technology, reshaping the very foundations of traditional financial paradigms. A prime exemplar of this shift is e-commerce finance. This isn’t merely about facilitating online transactions; it’s a holistic approach to supporting the entire digital commerce spectrum. From streamlined payment gateways to bespoke consumer credit solutions tailored for the digital shopper, industry behemoths like Alibaba’s Ant Financial and Amazon’s financial ventures are leading the charge. Harnessing the might of AI and big data analytics to craft hyper-personalized financial experiences.

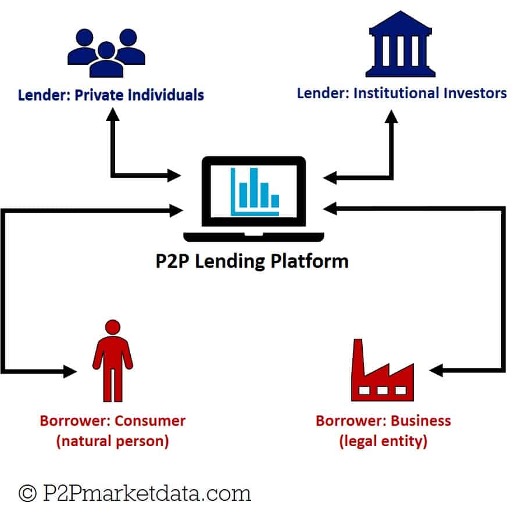

Venturing further, we encounter the realm of Peer-to-Peer (P2P) lending. This innovative model, sidestepping conventional banking corridors, fosters direct financial dialogues between borrowers and lenders on digital platforms . While the democratization of lending via platforms like LendingClub and Prosper is commendable, it’s not without its pitfalls, especially in regions where regulatory oversight might be playing catch-up . Yet, with judicious governance, P2P can redefine credit accessibility.

(Christensen, 2023)

Then there’s the phenomenon of crowdfunding, a mosaic of diverse models from reward-driven to equity-centric approaches (Klein, Shtudiner, &Zwilling, 2023). Names like Kickstarter and Indiegogo aren’t just platforms; they symbolize a paradigm shift in capital acquisition, where community endorsement and grassroots support take center stage.

Segueing into the domain of online wealth management, we witness the democratization of investment. No longer the preserve of the elite, digital platforms are demystifying complex financial instruments, catering to both the seasoned investor and the novice. The allure? A blend of convenience, transparency, and a user-centric ethos.

Rounding off our exploration, vertical financial search engines emerge as the unsung heroes, seamlessly connecting consumers with financial institutions. With platforms like Bankrate and NerdWallet offering a magnifying glass into the labyrinth of financial products, informed decision-making has never been easier.

(Patel, 2023)

To encapsulate, as we stand at the cusp of this internet finance revolution, it’s evident that we’re not just witnessing a change in services but a profound evolution in consumer financial behavior and expectations. And as this narrative unfolds, it sets the stage for deeper explorations into the subsequent facets of this digital financial odyssey, promising a tapestry of complexities and opportunities.

The risks associated with internet finance and the challenges in its regulatory processes

In the ever-evolving tapestry of the financial world, the digital metamorphosis of the sector stands out as both a beacon of progress and a cauldron of challenges. The allure of internet finance, with its promise of unparalleled convenience and streamlined efficiency, is undeniable. Yet, beneath this shimmering surface lie intricate webs of risks that demand our attention.

Foremost among these is the looming shadow of cybersecurity. As the financial pulse increasingly throbs in the digital realm, it becomes an enticing magnet for cyber adversaries. The fallout from data breaches isn’t just monetary; it’s the intangible yet profound erosion of trust in the very platforms that promised a financial revolution.

(Paul, 2023)

Navigating further into this digital maze, we encounter the regulatory conundrum. The rulebooks, crafted in the bygone era of brick-and-mortar finance, often find themselves grappling with the agile, nebulous nature of online platforms. The regulatory, often a step behind, risks either stifling the very innovation it seeks to foster or leaving gaps that can be exploited.

Then there’s the double-edged sword of democratized credit access. On one hand, it’s a triumph of financial inclusivity, breaking down traditional barriers. On the flip side, it’s a potential minefield of credit risks. The allure of easy access can sometimes overshadow the essential due diligence, leading to a precarious house of cards, teetering on the brink of defaults.

Amidst this, the inherent volatility of the burgeoning internet finance sector adds another layer of complexity. The market, still finding its feet, is rife with inefficiencies and disparities. The uninitiated investor or consumer, without the compass of accurate information, might find themselves adrift in this tumultuous sea.

Recognizing this intricate puzzle, regulatory bodies are in a perpetual tango with industry trailblazers, aiming to harmonize innovation with safeguarding measures. But, given the mercurial nature of internet finance, this is less a one-time solution and more an ongoing dialogue, demanding agility and foresight from all stakeholders.

To encapsulate, the narrative of internet finance is a blend of promise and prudence. As we transition from this segment into the subsequent facets of our exploration, it becomes evident that the journey ahead, while brimming with potential, requires a harmonized, vigilant approach to truly harness the benefits while mitigating the pitfalls.

The development recommendations for internet finance and its regulation

(the Federalist Society, 2017)

The digital tapestry of internet finance, with its pulsating rhythms of innovation and transformation, stands as a vivid illustration of the seismic shifts technology can induce in age-old sectors. As we traverse this labyrinth of online financial interactions, it becomes abundantly clear that to truly tap into its reservoir of opportunities, a meticulously crafted, informed strategy is indispensable. To chart a course through this multifaceted domain and lay the groundwork for a flourishing digital financial future, we must arm ourselves with a robust set of recommendations.

At the heart of our discourse is the clarion call for a nimble, visionary regulatory paradigm (de Kloet et al., 2019). The rulebooks of yesteryears, anchored in the certainties of traditional finance, find themselves at sea in the tempestuous waters of internet finance. Rather than clinging to these relics, we must champion a regulatory ethos that’s both prescient and malleable, one that can intuitively navigate the ebb and flow of digital finance. This monumental task demands a symphony of minds: the sagacity of regulatory stalwarts, the audacity of digital finance mavericks, and the acumen of tech maestros. Their collective genius can sculpt a framework that delicately balances the zeal for innovation with the sanctity of consumer safeguards.

Next in our strategic arsenal is the imperative to supercharge our risk management protocols. The digital footprints scattered across the internet finance landscape are treasure troves of insights. By harnessing avant-garde technological tools, from intricate data analytics to artificial intelligence, we can transmute this raw data into a strategic compass. This alchemy enables real-time fraud detection, razor-sharp credit risk assessments, and the agility to preempt market anomalies, crafting a bulwark against financial turbulence.

Furthermore, as the silhouettes of traditional and digital finance begin to merge, we stand at the cusp of an integrative revolution. This confluence can birth a symbiotic financial realm, melding the steadfast reliability of age-old banking bastions with the agility and user-centric ethos of digital trailblazers. A financial symphony that resonates with the aspirations of the modern user.

Yet, as we charter these unexplored territories, the beacon of consumer education and unwavering transparency must guide us. It’s incumbent upon digital platforms to demystify the arcane corridors of online finance, offering a guiding hand through resources and insights. A steadfast commitment to transparency, especially in the sanctums of data stewardship, fee structures, and potential risks, is the bedrock upon which trust is built, a trust that will determine the trajectory of internet finance.

Broadening our horizons, the borderless essence of internet finance beckons for a global camaraderie. Operating in isolated regulatory silos is a myopic strategy in this interconnected world. By weaving a tapestry of international alliances and dialogues, we can envision a cohesive regulatory mosaic that shields consumers and investors across the globe. This global consortium can also be the crucible for sharing pioneering technologies, best practices, and market foresights, heralding a unified digital financial epoch.

To encapsulate, the vast cosmos of internet finance, with its kaleidoscope of challenges and prospects, demands our astute attention. While its allure is magnetic, unlocking its treasure trove requires a harmonious blend of insight, strategy, and collaboration. As we conclude this exploration, it’s evident that with a holistic, synergistic approach, internet finance can metamorphose into a lighthouse of innovation, security, and shared prosperity in the global financial odyssey.